Please Kill Me: The Step Up in Basis at Death

Key takeaways:

When you inherit something when someone passes, it’s important to understand what you’re on the hook for to pay taxes on.

If you want to gift someone appreciated assets like stocks or real estate, doing so before you die might not actually be helping them out.

If you inherit real estate, stocks, collectibles, or other business interests, step-up in basis applies and you won’t have to pay capital gains tax on what you inherited.

Step-up in basis is one of the rare gifts in the tax code. You don’t apply for it. You don’t have to qualify. You just have to hold.

Let me explain: When you die, so do your capital gains. The intent behind step-up in basis is to remove a large tax burden from your heirs.

Usually, the tax code rewards action. File this form. Elect that status. Hit the deadline or pay the penalty. But every once in a while, it rewards you for doing absolutely nothing. Step-up in basis is one such case.

Let’s start with the basics of basis. 🙄

Basis is what you pay for something. Say, the purchase price of your house, the purchase price of a share of Disney stock your uncle bought for you when you were born, or the price of a watch.

If you die holding an appreciated asset—in other words, an asset that grew in value over time like real estate, stocks, or a business interest—the basis for that asset resets to its fair market value on the day you die. Your heirs inherit it as if they bought it at that new, higher price. The gains that asset made over your lifetime? Erased. No capital gains tax owed by you or the people who inherit your stuff.

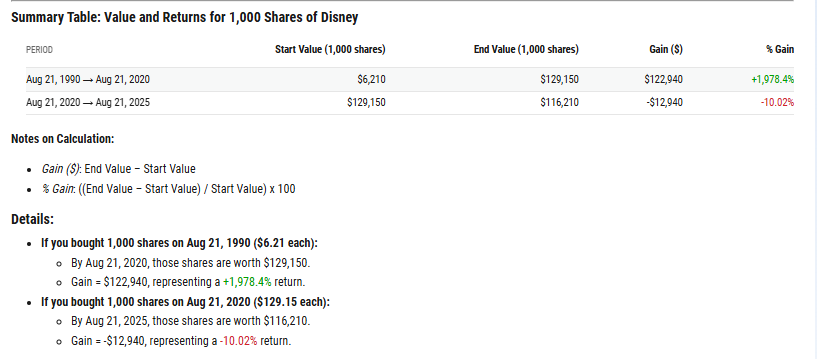

Let’s say someone bought a share of Disney on the day they were born on August 21st, 1990. Back then, the stock was valued at $6.21 a share. Tragically, this person passed away on their 30th birthday when the stock was valued at $129.15 per share. Their sister inherited the stock and her new basis is now $129.15. When the sister sells the stock five years later, the price is now $116.21, a 10.02% loss.

So with the step-up in basis, the sister actually gets to take a loss on her tax return, instead of paying capital gains tax on the 1,978% gain! Now imagine it wasn’t just one share purchased in 1990, but 1,000 shares!

Then the sister who inherited all 1,000 shares escapes capital gains tax entirely (which have rates between 0-20%) on more than $100,000 of taxable gains.

This happens automatically. You don’t need to elect anything special, but you should probably have an accountant and likely a lawyer help you manage the estate.

Here’s another example, but this time with real estate: Let’s say your dad bought a house in 1980 for $100,000. He dies in 2025, and you inherit the house. When you get it appraised, you learn that it’s now worth $900,000, and you decide to sell it for that same amount. There’s no capital gain—because your new basis is $900,000. You owe nothing. However, if he gifted you the house before he died, then you would have inherited his basis instead. Which means that you would have to pay the capital gains tax on the $800,000 taxable gain when you sell. The difference between understanding this rule and missing it is often six figures.

It’s best to make sure you’re all buttoned up with the IRS, so pay for a licensed appraiser to assess the value of an inherited home as close to the date of death as possible. Of course, you can use property tax records or even online references like Zillow, but if you end up needing to defend yourself to the IRS or someone’s lawyer, it’s most effective to have a certified appraisal done and keep the receipt of payment! This also applies to things like art and watches…get that shit appraised!

So what kinds of assets qualify for the step-up? Things like real estate, taxable brokerage accounts, individual stocks or mutual funds, collectibles, or business interests. Assets that don’t qualify include IRAs, 401(k)s, annuities, pensions, and regular bank accounts. Those pass to heirs with the original cost basis intact and often with taxes still owed by the estate.

The step-up in basis rule was not invented as a clever tax loophole; it was born out of the early U.S. tax system and a very old problem: how do you tax assets accurately when ownership transfers at death? The provision was first introduced in 1921, just a few years after the federal estate tax became law in 1916. At that time, lawmakers were trying to reconcile two different taxes applied at death—the estate tax itself and the income tax on unrealized gains from investments that haven’t been sold yet—without making heirs pay twice on the same appreciation. Step-up in basis was Congress’s solution: reset the basis to fair market value at the time of death so that heirs wouldn’t have to owe capital gains tax on gains that had effectively already been captured for estate tax purposes.

Another practical driver for instituting the step-up in basis was record-keeping. Before digital records and modern broker statements, tracing what someone paid for farmland, stocks, or a home purchased 40 or 50 years earlier was often impossible. Stepping the basis up to the current market value simplified compliance and avoided endless disputes over ancient purchase prices (ahem, or in some cases, stolen).

But this rule hasn’t always stood unchallenged. In the late 1970s, Congress briefly replaced step-up with a carryover basis system, where heirs inherited the original cost basis instead of a stepped-up one. That change proved so unpopular (largely because reconstructing decades-old basis was a nightmare in practice) that it was reversed. Step-up returned and has stayed ever since.

In recent years, proposals to repeal or reform the rule have surfaced but none have passed. Those proposals often hinge on the same debate that kicked off nearly a century ago: should heirs avoid capital gains on inherited growth, or should that appreciation be taxed at least once in someone’s lifetime? The calls for reform of the step-up in basis revolve around just how high the estate tax exclusion has climbed. In 2017, before the Tax Cuts and Jobs Act, a single person dying could exclude about 5.5 million of wealth from the punishing 40% estate tax. But with the TCJA law changes in 2018, that exclusion doubled to 11 million. So overnight, about 5 million dollars in untaxed income opened up for wealthy families.

Being Married Rules (Especially in California)

If you’re married, it gets even more interesting. In community property states, married couples each own 100% of most assets acquired during the marriage. That means when one spouse dies, the entire value of their shared assets can receive a full step-up in basis. Not just half. So if you and your high school sweetheart buy a home together in your 20s for $200,000 and your spouse tragically passes away at 50 and the home is now worth $600,000 at their death, your basis is now the full $600,000 and you could sell it next year and pay zero tax because there is no gain.

The nine community property states are Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. A few others like Alaska, Florida, Kentucky, South Dakota, and Tennessee, let you opt into community property treatment through a special trust. But everywhere else, the rules are different. In common-law states, only the deceased spouse’s share of jointly owned property is stepped up. The surviving spouse keeps their original basis.

That distinction can mean tens of thousands in taxes depending on when and how the surviving spouse sells. I’m honestly shocked there aren’t more step-up-in basis motivated mariticides or uxoricides1 in community property states.

Understanding how, when, and where step-up and basis works matters because sometimes people try to be smart, and sometimes outsmart themselves. For instance, they’ll gift appreciated assets to a loved one, thinking that they’re helping. Or they sell an appreciated asset early to “clean things up.” They assume that giving things away while they’re alive is the generous move, without realizing that they’re handing over a giant future tax bill in the process.

The step-up-in basis to reduce capital gain taxation only works if the asset actually passes the way you think it will. Step-up in basis is a tax rule, not an estate plan. It doesn’t decide who gets the house, who controls the brokerage account, or whether your kid, your spouse, or your estranged cousin ends up owning the thing in the first place. That’s why wills and trusts matter. They’re not just about drama prevention, they’re about making sure the right person owns the asset at death so the tax rules can do what they’re supposed to do. A step-up is powerful, but only if the property lands where you intended. So get your estate plan done, this week! Otherwise, you could optimize the taxes on an asset you accidentally gave to the wrong person.

Parting shot: You can’t take it with you, but you can decide how painful it is for everyone else.

Thanks for this great article, so many people are unaware of step-up basis and why transferring assets during life is not necessarily the wisest thing to do. With my own mother I saw a curious phenomenon take place, which is that she became increasingly unwilling to sell assets that had a low cost basis because she saw the opportunity of her death to reset the ledger. This meant she died with a wildly un-diversified portfolio that could have financially ruined her had the asset depreciated - diversification would have been expensive, but it's what any financial advisor would have recommended (and many did). Luckily the asset did not depreciate but grew. Once she died we all sold it and diversified, and I think she would be pleased to know that a position she inherited from her father and held for almost 50 years, through multiple splits and acquisitions, created financial security for her kids.

So helpful, as always!