Stop Throwing Your Money Into the Void: The Savings Order of Operations

A choose-your-own-adventure financial plan

Key Takeaways:

If you have access to a 401(k), it’s almost always a good idea to contribute to it, even if it’s just 1-3%

Use the Savings Order of Operations to figure out where you land and let this simple tool direct your next dollar.

If you have high-interest credit card debt, throw everything you’ve got at eliminating it.

The world of personal finance is governed harshly by iron-clad rules of thumb. I don’t think that’s a bad thing. As humans, we need goals, restrictions, guidance, whatever you want to call it, when it comes to understanding money. Most of us don’t have a full grasp on the lifetime value of a dollar so we default to the easiest thing: We spend it on something nice.

So we could all use some basic guidelines to help us not only keep, but also increase our pile of money, rather than just spend it on the next fun thing you spot on Instagram. Here are some iron-clad rules of thumb that I like to follow:

Spend less than you make

Save 20% of your income

Have an emergency fund of 3-6 months of living expenses

OK, so maybe you’ve heard all this before. This isn’t exactly groundbreaking advice. Today’s newsletter is not a clickbaity opinion piece1. However, even with all this practical advice, it’s hard to know where to begin. Should you just stop buying eggs, lattes, and avocados and put that money into your emergency fund instead? Should you move and find a cheaper apartment? Should you start making and bringing your own lunch to work? Should you prioritize building up your emergency fund or contributing to your 401(k)? Don’t worry, I’ve got you. What follows is an easy walk in the park through one of the most important rules of thumb we have in personal finance: The Savings Order of Operations.

I wish that every person could sit down with a trusted personal finance expert, who is a fiduciary2 and get tailored answers and a custom financial plan. The economics of this, unfortunately, don’t make sense for most people early in their careers or facing hardship. As a business owner, I’ve tried to serve everyone who needs help, but it just doesn’t work. Maybe someone will figure this out someday, but the financial services industry isn’t there yet. AI might help, but it’s not going to solve the issue of a human needing support and guidance through creating new spending and saving behaviors and not doing something drastic when the market moves.

So, for now, we’ll have to rely on The Savings Order of Operations; it’s a simple framework to determine where your next dollar is best saved. Think of it as your very own financial advisor, or a “choose your own savings and investing adventure.”

It’s impossible for me to make recommendations that fit everyone because every person is different. Some people (like business owners and freelancers) need to keep more cash on hand because their income can be irregular. Some people need to have more savings sooner because their career is physically demanding, and they won’t be able to work as long.

However, in our work with clients at Brooklyn Fi, we’ve used this savings order of operations for years, and it works pretty well for most people.

Should You Pay off Debt or Fund Retirement Accounts: The Answer is Both

This either/or debate comes up all the time with my clients and readers. You may be thinking something like, “I know I need to prioritize paying down debt or funding my emergency fund, but I also want to save for my future. Should I do both?” Yes, you should. As we’ll see later with our Meredith case study, you can invest for the long term AND build up temporary cash reserves at the same time.

Unfortunately, people fall into the neverending cycle of trying to save money, but their savings accounts just keep getting emptied. They build up, and then they tear down. And trust me, it’s usually not something as trite as a shopping habit that’s causing it, it’s usually a traumatic life event or a minor inconvenience out of our control that keeps us on the hampster wheel of never being able to break the cycle. If this is you, let me be blunt: you need to make a change. What you’re doing isn’t working. Ask for help, and get accountability from a trusted friend or professional. Break the curse.

This is apropos of nothing, but I just have to say it: I’m personally not a fan of rushing to pay off your mortgage or low-interest loans, but feel free to ask me about it sometime.

The Savings Order of Operations

Think of this process like a huge bucket of water (the money or income) being poured into another empty bucket. When that second bucket is full, the water spills over into another empty bucket, and so on. If you have no debt and a fully-funded emergency fund and there’s $10,000 extra available for you to save, then that $10,000 overflow of money should fill up the “Max out 401(k)s" bucket a little less than halfway (since the maximum amount you can contribute to a 401(k) in 2025 is $23,500).

But let’s do something a little sexier than buckets. Let’s tap into one of my great passions: science fiction. One of the great works of the modern sci-fi era is Leviathan Wakes by James Corey. If you like sci-fi, read it, it’s a masterpiece. Or there’s also a TV show they made out of it called The Expanse, which I have watched a full five times. (There are 6 seasons).

Anyways, on the show, they have these things called “ring gates” which are giant rings of energy floating in space that can do really weird things to ships when they fly through them, like transport you to other worlds. (I’m gonna land this spaceship on personal finance planet, I promise.)

So instead of the buckets, think of the savings order of operations like a spaceship flying through ring gates in space with a forcefield. And the forcefield won’t let you pass through the first ring until you complete the mission: pay off your high-interest debt.

Here’s the Savings Order of Operations:

Pay off High-Interest Debt

Dollar amount: It depends.This is credit card debt with an interest rate of 10% or higher. If you have credit card debt, focus on paying that off first. That high interest rate is crushing you, throw everything you’ve got at the problem.

Fund Emergency Fund with 3-6 Months of Living Expenses

Dollar amount: It depends.

For most people, $15k-$50k is a good target.Find out how expensive you are and keep 3-6 months of living expenses in an online high-yield savings account.

Max out 401(k)s (or 457s or 403b)

Dollar amount: $23,500 in 2025, $31,000 if you’re over 503. Some people may have the privilege of contributing more.

If you have one of these through work, max it out. If you’re a business owner, start your own Solo 401(k) or SEP-IRA. In other words, build up your “Don’t you dare f*cking touch me” long-term retirement savings.Max out Roth or Traditional IRAs

Dollar amount: $7,000 in 2025, $8,000 if you’re over age 50.The maximum contribution for IRAs is $7,000. Proceed with caution because of income limits on Roth IRA contributions. Whether you can deduct any IRA contributions is dependent on the income number on your tax return, ask your accountant4.

Max out HSA

Dollar amount: $4,300 for one person, and $8,550 for a family.

If you have access to one of these through your healthcare plan you can fill up this bucket and actually invest the money you have in this account in the stock market for future use for medical expenses. (Watch out for FSAs, those are not investment accounts and you must spend any money you put in an FSA account within the year on medical expenses.)Fund 529 College Savings Plan

Dollar amount: It depends. $10,000 is the full amount a married couple can deduct from their taxable income in New York State.

These nifty accounts have all of the tax-free growth benefits of IRAs! And in some states, your contributions are tax-deductible. If you can manage it, put $10k a year into this if you plan to have children or pay for a family member’s college education.Invest a Set Monthly Amount in a Taxable Brokerage Account

Dollar amount: It depends. When in doubt, do $2,0005.

This is your fuck-off medium-term savings fund. I like to do 5% of my take-home pay—this can be anywhere in the range of $100-$10,000 monthly. Automate these contributions!

Finally, if and ONLY if you’ve done everything above, may you progress to the final action.

Alternative Investments and/or Charity

Dollar amount: It depends.

Donate to charity, invest in your friend’s bar, invest in an alternative asset like crypto, or buy real estate. I don’t care what you do with it, it’s your money.

Me, Dall-E, and Canva had a fun time with this one:

Meredith: Building with Confidence

Meredith is a software sales associate who makes $85,000 a year. She has $3,000 in her savings account, and her emergency fund goal is $15,000. She’s contributing 3% of her salary to her 401(k). Right now, she’s feeling a little overwhelmed because she keeps spending her savings. She’s considering turning off her 401(k) contributions to focus on building her emergency fund faster.

Meredith, don’t do it! Automating savings into your 401(k) is one of the best financial habits you can develop, and if your employer offers a match, that’s free money you don’t want to leave on the table.

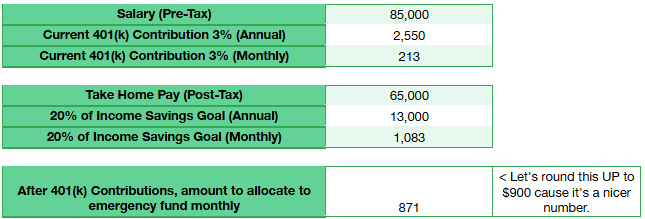

Again, these are rules of thumb that can be bent. Let’s say Meredith’s taking home $65,000 a year after taxes (I did some quick tax math) and is dedicated to saving 20% of her income (she’s read my Substack 🫡). So she’s got $1,083 to allocate to savings each month. We really need to build up that emergency fund and she could do it in a year, but I don’t want her to stop contributing to “long-term don’t fucking touch me savings.” So we’re going to keep putting 3% of her salary into her 401(k) and set up automated contributions of $871 a month to her emergency fund. She’s already got a $3,000 head start towards her goal of $15,000, so it will take her about 14 months to get there! Once she hits that goal, she goes back to the savings order of operations and re-directs that $871 a month to her 401(k). But $871 is a weird number, so let’s round it up to $900 and find somewhere in the monthly budget to save $29.

Let’s look at the numbers in a chart for clarity. Note: I promise I’m not trying to confuse you here. 401(k) contributions are typically looked at as a percentage of PRE-TAX income. However, I want you to be aggressively saving 20% of your POST-TAX/take-home pay. The numbers get a little jumbled because your 401(k) contributions are tax-deductible but when in doubt, save 20% of your take-home pay.

Jack: 401(k), Let’s Go!

Jack is a designer making $130,000 a year. He has no credit card debt, a solid $30,000 emergency fund, and is already contributing to his 401(k). Following the savings order of operations, he starts methodically filling up the next bucket: maxing out his 401(k) contributions to the 2025 limit of $23,500. He won’t get the full $23,500 contribution, but that’s okay!

Jack is in a great spot—he’s secured his financial foundation and is steadily building long-term wealth. He still has disposable income left, but instead of rushing into riskier investments, he stays patient and follows the plan. He’s tempted, of course - mostly by crypto. His friends talk about how much money they’ve made in the space6. If Jack wanted to throw a few hundred dollars or even 1% of his income into a riskier investment, I don’t think the Savings Order of Operations police would arrest him. :)

With New York City + New York State + Federal taxes, following our rule of thumb of saving 20% of your AFTER-TAX income, you’d have to make at least $170,000 in income to be able to save the 401(k) max of $23,500 per year. That’s depressing. But also a good reminder that income is the foundation of wealth creation. Prioritizing a higher income and higher savings rate is what most people in this country will need to do to be able to stop working at some point and have a comfortable retirement.

Elizabeth: Dominating the Savings Order of Operations

Elizabeth is a tech executive making $300,000 a year, she’s a client of my firm, for sure. And if she isn’t, she should be. She’s maxed out her 401(k) already, but she makes too much money to contribute to a Roth IRA and she knows her Traditional IRA contribution won’t be tax deductible7. Now she’s sitting on extra cash and wondering what to do with it. She doesn’t really have a clearly defined goal. She’s 33 and doesn’t have children. She likes renting and isn’t sure if she wants to stay in the city long-term. Let’s see how she moves through the savings order of operations.

Here’s where things get interesting:

Pay off High-Interest DebtFund Emergency Fund with 3-6 Months of Living ExpensesMax out 401(k)sMax out Roth or Traditional IRAs

She’s going to max out her Roth IRA, but she’s going to use a sneaky tax loophole called the back door Roth IRA. She’ll contribute the $7,000 to her Traditional IRA and then convert it to a Roth IRA (under the supervision of her financial advisor).Max out HSA

Meredith’s company has a very attractive benefits plan that allows her to have a very low deductible. Because of this, she doesn’t have access to an HSA.Fund 529 College Savings Plan

She isn’t sure if she wants to have kids, but her friend AJ who writes this newsletter, convinces her that this is such a valuable tax savings bucket to fill up even if she’s not going to have children. Plus, she can use it to help out her adorable nephews with college. Because she’s not sure, she’s going to start up a reasonable $300/month automated contribution to a 529 plan. Fast forward to 5 years later when she’s basically forgotten about this account: she’d have $18,000 principal in there plus compounding.Invest a Set Monthly Amount in a Taxable Brokerage Account

Elizabeth is living her best life in New York. She loves to travel and is taking some big trips this year. She wants to be aggressive about savings. I’d push to start with monthly contributions of $2,000 automatically withdrawn from checking right into her taxable brokerage account. If she sees her checking account not being able to cover her credit card bill, then we know she’s being too aggressive with savings and she can always reduce this contribution. When she gets a performance bonus at work, her financial advisor has trained her to immediately direct it to this account.Alternative Investments and/or Charity

Through her job, she has access to exciting investment opportunities. Her financial advisor typically steers her away from these risky investments because while she does have a healthy income, Meredith’s future is so uncertain so the best thing she can do is shore up her long-term savings. That said, picking stocks of companies she reads about is appealing. She finds it fun. She knows it’s not too serious and doesn’t care if her investments lose most of their value. She decides to take $2,000 and put it in a “sandbox” brokerage account so she can buy and sell individual stocks (just for fun).

The Power of Automated Savings—and Navigating the Unknown

The best part about the savings order of operations? It’s like a well-plotted course through the ring gates in The Expanse—a way to move forward without getting obliterated by unexpected asteroid fields.

But if you’ve seen the whole series or read all of Leviathan Wakes, you know that just because you can go through a ring gate doesn’t mean you should fly in at full speed with no plan. Automating your savings is like setting your ship’s trajectory—it keeps you moving in the right direction. And just like in space travel, sometimes the map changes. Life throws curveballs. Your goals shift. The market does something weird. That’s when you reassess, tweak the plan, and keep going.

Follow the plan, automate what you can, don’t turn off those 401(k) contributions, and when life inevitably throws something unexpected your way, adjust your course—but keep flying.

Parting shot: Having a clear, yet flexible plan when it comes to savings, means you’ll continue to grow your wealth in a variety of ways to give you a nice, fluffy cushion for a wide range of savings goals.

The best $20 I spent this week: I am a sucker for packaging. I love the St. Agrestis non-alcoholic Negronis. They have the best name: Phony Negroni. They come in a beautiful white limited edition version.

I wrote a good one of those about picking the right romantic partner.

A fiduciary is someone who puts your interests ahead of their own at all times and doesn’t take commissions or kickbacks.

Weirdly, if you’re age 60-63 you get this extra catch-up contribution limit. Congress is weird, I don't make the rules. Read about it here.

My DMs usually blow up at the end of the year from my business owner friends asking me how to undo IRA contributions because they made more money than they thought.

Don’t ask me how I came up with this number. It’s a nice number. Do more if you can. Do less if you can’t

They haven’t actually made money yet; they just see balances in their account. Holding crypto is one thing; selling it is another.

Here are the income limitations on IRAs from Schwab.

Gosh I really love and appreciate your writing! These are fantastic primers and as someone newly making a high income (after years of training and barely scraping by) so beyond helpful!

I am always interested in the ways people approach threading the needle between these overarching rules of thumb (that push most people in the general right direction) and communicating the inherent nuance of planning. Before I started working in the personal finance space, I really liked the easy steps to follow, that places like Personal Finance Club (https://www.personalfinanceclub.com/how-to-prioritize-your-money-the-phases-of-investing/), the White Coat Investor (https://www.whitecoatinvestor.com/financial-waterfalls-for-new-residents-and-attendings/), and this post lay out. Now, I am more wary of them.

I wonder (if you'd be willing to share!) how you think about combining the psychology and math of personal finance into this order of savings as well as your public writing in general.