Fortune Favors the Adaptable

How to Set Savings Goals That Work During The Good Times and The Bad

Key Takeways:

Money moves in cycles – Expect highs and lows, and build a system that works in every phase.

Always be saving – Whether you’re struggling, fine, or rich, there’s a version of saving that works for you.

Life’s a cycle, not a straight line – Financial security isn’t about never struggling—it’s about knowing how to adapt when you do.

They say that writing about music is like dancing about architecture1. Writing about money is a similar absurdist endeavor. I find myself like a doctor writing prescriptions for imaginary people with imaginary ailments I’ve never met. I don’t know if you’re in debt or secretly sitting on an inherited real estate empire. I’m trying to help you, my reader, but I don’t know anything about you.

The problem with writing about money and trying to give people guidance is that it’s so deeply personal and one’s relationship to money can change in an instant. It’s where we are born, who our parents are, and where we go to school. It’s the life choices we make–who we do or don’t marry, what career we choose, and whether we have children that can have a dramatic impact on our lifestyle and ability to build wealth.

Some things may change our financial situation overnight: finding out you’re having twins, finding out the company you work for is going public and your stock is worth hundreds of thousands of dollars, the death of a relative makes you a millionaire overnight, or something as terrible as suddenly losing your spouse and not having any life insurance leaves you down the love of your life and without an income to support your family. I find that writing about money is either deeply personal or distant and prescriptive.

This advice tends to be delivered in two ways. The first bucket is the “this happened to me and here’s how I overcame it” type of personal advice, which usually consists of people sharing stories about paying off debt with a radical new hack, starving themselves of pleasure and social interactions to save all their money to retire early, or surviving a terrible tragedy and getting through the other side. The second bucket is the “do this, not that,” prescriptive kind of advice.

With this newsletter, I’m trying to do something more in the middle. I want to share a perspective about money that makes my readers feel like they can improve their situations but also have the advice feel palatable and somewhat enjoyable to read.

Like many writers, I suffer from the brutal affliction of crippling self-doubt and being self-absorbed at the same time. I love attention but I fear how I’ll be judged. So with my last few posts I’ve felt like I’m drowning a bit in the second bucket of “do this, not that” advice.

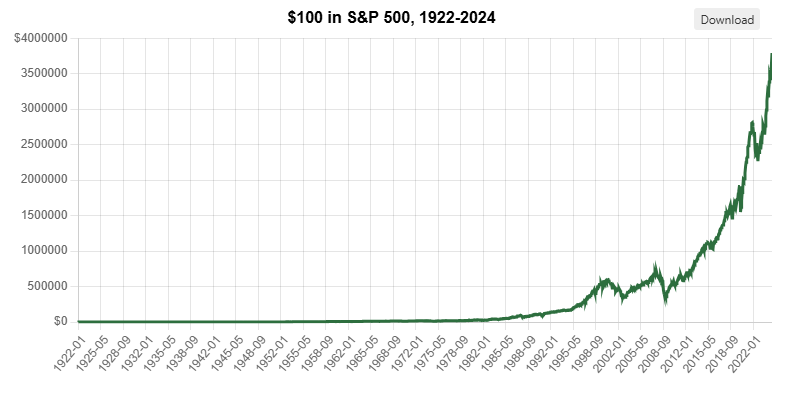

So today, I’d like to dip into the first bucket of “this happened to me and here’s how I overcame it” and share a little bit about my own financial journey and how it’s shaped a theory I have about how to move through life as your financial circumstances fluctuate. My hope for you is that your financial circumstances mimic the history of the US stock market, meaning it only goes up and to the right.

That’s a nice picture isn’t it?2 If we zoom out on 100 years of the stock market, the trend line goes up and to the right. But what we don’t see are the dips along the way - the 1933 great depression, the 2008 financial crisis, the 2020 start of Covid. This graph line could be analogous to your life - a job loss, a sick parent, a miscarriage, a divorce, an illness, or a really shitty bout of depression - things that are setbacks and truly terrible in the moment but in the zoomed-out trend graph of your life could look like minor setbacks. Our economy is cyclical: big bad event happens, economy is bad for a while, government comes in and makes it easier with lower interest rates, economy comes back, economic boom times, things get too expensive, then economy crashes. Or something like that. Life is similar. One devastating breakup could lead to meeting your real soulmate. Getting laid off from your dream job could lead to starting the company that changes your life.

Once you understand that life is cyclical, you will be happier and richer.

I’m going to say that again: once you understand that life is cyclical, you will be happier and richer.

Hard times happen. But they are just that, times. Hopefully brief periods that may last a few weeks, months or years. But hard times (for most of us not living in abject poverty) don’t last a lifetime.

Savings Plans for Good Times and the Bad

It’s important to have a range of savings plans to move between: rich, fine, and struggling- that way, you’ll always be saving. For example: If you lose your job or finances are tight, then you can default to your “struggling” plan. If you got a new job with a big new salary, then move on up to your “rich” plan.

Life is twisty and turny and as humans, we adapt. Sometimes you reach into your bag for a lipstick and you get stabbed by a safety pin. But when it comes to money, we get so fucked up about it that we don’t adjust quickly enough to survive temporary pain. I want you to think about your spending and savings habits as three different flavors: Struggling, Fine, and Rich. I’ll describe each one to you, but I also want you to define each one for yourself since we’re all such unique weird little pieces of shit.

Struggling: You are living very close to the edge. There never seems to be enough money coming in. There’s debt, some of it you owe to credit card companies.

Fine: You’re doing fine! You’ve got a nice healthy income and you’re able to build up some savings. Saving for the future is something you’re doing regularly.

Rich: You’re doing great. You have financial security. You may or may not be financially independent but something pretty dramatic would have to happen for you to get thrown off track. You’re saving a significant portion of your income, or investing a windfall and shoring yourself up for the future.

The concept here is that throughout your life, you will likely experience cycles of these three modes. Periods of fine followed by some struggling. Perhaps an era of rich is followed by a year or two of struggling due to a divorce or job loss. You embrace the change, you are unphased by it, you stick to your financial plan and keep saving, through the good times and the bad. You have a solid savings plan for each state, and you can move easily between them. A setback becomes just that, something temporary you know you just have to knuckle through. Your struggle has an endpoint. You can bounce easily between these savings plans without taking your eye off the target of financial independence. You set up good habbits that don’t get interrupted by setbacks that are out of your control.

Struggling

In my 20s I worried about money a lot. Just out of college and working my first editorial job, it was so stressful just to have enough money to pay rent and buy groceries that I often ended up in tears when I overdrafted my bank account. I was simply not making enough money to support my lifestyle. I lived in New York City and had chosen a career in book publishing, which is known for its hilariously low salaries. I had “affordable rent” and I really didn’t have many expenses. I had student loans to pay off and weird health problems that kept coming up (in hindsight, perhaps related to my anxiety around money?) I wasn’t actually spending that much money, I just wasn’t making enough to cover my living expenses. Don’t get me wrong, I had a great life. I went out with friends often and had interesting romantic relationships. I saw a ton of live music, and movies and went to parties. I did well at work and got promoted. I took the subway and walked everywhere, this was before Uber and a taxi home from a party was an extreme luxury reserved for very late nights. I wouldn’t trade that time for anything, truly. But perhaps I’m viewing it through rose-colored glasses. Dinner out with friends meant a splurge at Vanessa’s Dumplings or the $12 brunch at Harefield Road. I meticulously meal-prepped and side-hustled (I even wrote about meal prepping for money).3

I shopped in Chinatown after work to find the absolute cheapest ingredients. I got my work lunch meal cost down to less than a dollar by eating cold soba noodles with scallions. Delicious and less than $1 per serving! I supplemented my income with second jobs. I was a bar-back for one summer which paid really well but was so exhausting on top of a 9-5. I wrote for online magazines like Refinery 29 and Saveur for a few hundred dollars a story.

At one point I moved in with a boyfriend from a wealthy family. I don’t remember how we split the rent but I do remember a very important piece of advice he gave me: start automating contributions to your savings account. I was incredulous because I was already living so close to the edge of overdraft every month. “Just do $100 a month, then you’ll have $1,200 by the end of the year.” That was pretty good advice. I was also contributing to my 401(k) at work because on my first day, I peered over at my cubicle neighbor and asked them what to do. They said something like “Put in 6%, then you’ll get free money from the company.” I listened. This was 2010, we were coming out of the 2008 financial crisis. I just felt lucky to have a job when so many of my college friends couldn’t find employment, so they moved back home or went to grad school. That wasn’t an option for me, I had decided. I would make it in New York even if it was hard. Knowing I could always move back in with a parent was a nice safety net. Knowing someone could bail me out if things got bad was a privilege I’m grateful for.

What does struggle look and feel like to you? Imagine a time in your life where money was a source of stress and there never seemed to be enough of it. Maybe that’s your current reality?

So how do you plan for a future when you’re barely surviving the present? How do you save money for some unknown future when a dollar now could buy a simple pleasure or a little comfort?

How to Save When You’re Struggling

The answer is that you establish a savings practice (a foundation, if you will) and that you don’t worry about the numbers or the percentages, you just do what you can, even if it’s the bare minimum. My advice here is that you need to have two streams of savings: one into your long-term “don’t fucking touch me 401(k)” and the other into your temporary emergency savings.

If you have access to a 401(k), you should do the bare minimum, which is usually 3% to get your employer match. If that’s too much and your paycheck shrinks, go down to 1%, but don’t shut it off. If you don’t have a 401(k) through work, make your own investment account named “401(k)” and treat it like one.

Next, you’ll need to set up automated savings to a high-yield savings account at a different bank. Start with $200/month transfers from your checking account to your high-yield savings account and set those transfers to recur every two days after your second paycheck hits, that’s when you’ll be least likely to miss that money. If $200 is too much, dial it back down to $100. If you are an overachiever, try $300 and see what happens.

When you’re in struggle mode your main objective is to keep as much of your money as possible. Do not let it slip through your fingers. I find the best way to do this is to gamify not spending money. Or at least that’s what worked for me. Have no-spend Sundays and Thursdays where you literally try to spend $0. See if you can do it. Try to get your average cost per meal down to below $10.

How to Save & Spend When You’re Struggling

Set up solid automation habits, even if the amounts are small – If you have access to a 401(k), contribute 1-3%. Set up automatic transfers from checking to savings of a small amount you can afford AFTER your paycheck hits. If you need me to give you a number, let’s do $200.

Don’t make spending mistakes – An Uber to a meeting you’re running late to can cost you. A late payment fee will ding you $25. These small things add up. Be vigilant about eliminating waste from your daily routines.

Reward yourself in unexpected ways – Don’t fall into the “treat yourself trap” and continuously undo your practiced behaviour with over the top rewards. Find small ways to treat yourself that don’t cost money: take a luxurious day of re-watching 30 Rock on the couch.

Fine

Then one day you wake up, and everything is…fine? Well, fast forward through switching jobs a few times, finding a company with a better business model, and just being a little bit older and wiser. You have a salary that covers your basic needs comfortably. You start to go “upstate” with friends on the weekend.

You’re no longer on the edge of an overdraft-induced panic attack, and your worries about not having enough money are no longer a Babadook under the bed. Your salary is covering your basic needs and then some. Maybe you’ve even gotten a raise or a bonus, or you finally landed a job that pays what you’re worth. You’re a tadpole that made it upstream and out of the pool “just out of college first-jobbers.” Your job title no longer says associate, it says senior-something or vice-something. You’ve got a little breathing room. This is where I found myself in the spring of 2017 - freshly promoted at a tech job I loved that paid me well. And it completely changed my life.

To make a very very long story short: I looked for advice for what to do with my new riches (having a little left in my checking account), didn’t find anyone good talking about money so I started a podcast, met my business partner, went back to school, started a financial planning firm, and here we are. We’re safe from the Babadoks and the two digit bank balances.

Financial security is so freeing. It’s like taking a cold drink of water after a long walk. It’s refreshing. I like the way Virginia Woolf talks about financial freedom in A Room of One’s Own.

“It is remarkable what a change of temper a fixed income will bring about. No force in the world can take from me my five hundred pounds. Food, house and clothing are mine for ever. Therefore do not merely labor and effort cease, but also hatred and bitterness. I need not hate any man; he cannot hurt me. I need not flatter any man; he has nothing to give me... Even allowing a generous margin for symbolism, five hundred a year stands for the power to contemplate.”

Ms. Woolf speaks so eloquently of the power of having enough income to cover your basic needs and a little extra to allow you the freedom to pursue your passions. Your hatred and bitterness goes away! Five hundred pounds4 a year gives us the power to think! God, I love her so much.

But what does fine look like in the modern age? You can go to dinner with friends without running the numbers in your head every time you order a drink. You’re not afraid to check your bank balance. Maybe you have an emergency fund that could cover a couple of months of expenses, and when an unexpected cost pops up—like your iphone shitting the bed—you don’t have to go into a full spiral.

But fine is also tricky because it’s where lifestyle creep lurks. When you have more money, it’s easy to find new ways to spend it—nicer restaurants, spontaneous weekend trips, upgrading your apartment. And honestly? Some of that is okay! The point of having money is to improve your life. The trick is to let your spending grow in a conscious way while still taking advantage of your new financial stability.

With my newly discovered financial stability at my tech job, I was firmly entrenched in the “fine” lifestyle. But that’s when I discovered this whole thing called the Financial Independence Retire Early movement which says you should aggressively save half your income. So I slipped back into my struggling mindset. I truly lived on rice and beans for a while and was contributing 50% of my salary to my 401(k) to catch up for previous lack of contributions. It was shitty, but I liked the sense of control it gave me. For the next few years I would shift back and forth between struggling and fine. Once I started a business, it was just a few years of struggle before I was suddenly fine again and making more than I had as a tech employee. Oops, it worked! Then we decided to invest back into the business and build a piece of software, then oops, there goes my fine money, back to struggling. You get it.

How to Save & Spend When You’re Fine

Automate your savings and investments – If you were saving 3% in your 401(k) when you were struggling, bump it up to 6%. If you were saving $100 a month in your emergency fund, increase it to $300 or more until you have at least three to six months of expenses saved.

Start investing outside of retirement – Open a brokerage account and put a little extra into index funds. It doesn’t have to be much, but getting in the habit of investing beyond your 401(k) will make a huge difference down the line.

Enjoy your money—but with guardrails – Give yourself permission to upgrade your life a little, but don’t let your spending expand to the point where you’re still living paycheck to paycheck. Pick a few things that really bring you joy (travel, guitar pedals, golf lessons, skincare) and let yourself indulge while keeping an eye on your big-picture goals.

Rich

At some point—whether through years of good financial decisions, a big career move, or a lucky break—you find yourself in rich mode. This doesn’t necessarily mean you’re rolling in millions, but you have financial security and a solid path towards not having to ever work again. You don’t have anxiety around money. You’re saving for retirement aggressively. You could buy a home if you felt like it. If you lost your job, it wouldn’t be a crisis—it would be an inconvenience. Setbacks become blips. Annoying pieces of lint you pick off your navy blue blazer.

Being rich is about optionality. It’s the ability to make choices based on what you want, not just what you need. Maybe you take a sabbatical, switch to a lower-paying job that brings you more joy, or invest in starting your own business.

How to Save & Spend When You’re Rich

Max out tax-advantaged accounts – At this stage, you should be maxing out your 401(k), IRA, and HSA if you have one. Take full advantage of every tax break available.

Build generational wealth – Start thinking long-term. This could mean funding a 529 for future kids, investing in real estate, or setting up a donor-advised fund if philanthropy is important to you. Go back to the savings order of operations.

Take calculated risks – Once you have a strong financial foundation, you can afford to be more aggressive. This could mean investing in a business, angel investing, or even taking some fun risks, like buying a vacation home or taking a year off to travel. You can also spend more on what makes you happy.

Money is Cyclical, So Plan for the Cycle

No matter where you are—struggling, fine, or rich—understand that this is just a phase. Your finances will ebb and flow over time. If you lose a job, if the market crashes, if you go through an unexpected life change—it doesn’t mean you’re doomed forever. It means you need to shift into a different gear.

Having multiple savings plans in place means that no matter what happens, you’re always saving something. When you’re struggling, you save a little. When you’re fine, you save more. When you’re rich, you go all in. The key is to build a system that flexes with your life—so you never feel completely off track, no matter what phase you’re in. Having an emergency fund, or simply a small stock pile of cash in the bank for emergencies, is absolutely the best way to shorten your time spent in the struggling phase.

And that’s how you keep moving forward, no matter what life throws at you.

It’s just a phase. I had blue hair in high school, and now I play golf during the work week.

Parting shot: Know yourself in all your modes and move effortlessly between them.

Best $20 I spent this week: I fired up my New Yorker subscription again. One of you told me to read this article about nuns working to save women on death row, and it’s one of the best things I’ve ever read.

Martin Mull may have said this first.

Source: S&P 500 data.

I apparently also wrote about how to make a pumpkin keg in 2016, but I have literally no memory of doing this or writing this.

I did a little shoddy inflation caluclator and came up with the figure of about $12,000 annually in today’s dollars. Sheesh, cost of living has certainly gone up.

I loved this post and it helped to normalize the reality of the financial life! Can you recommend some high yield savings account?

Loving your writing and podcast. “If you don’t have a 401(k) through work, make your own investment account named “401(k)” and treat it like one.” That is hilarious, and helpful!